The greater demand from society for influential organisations to be more socially responsible towards their communities and fans has seen gambling lose its status as the most common primary sponsor among team sports in England.

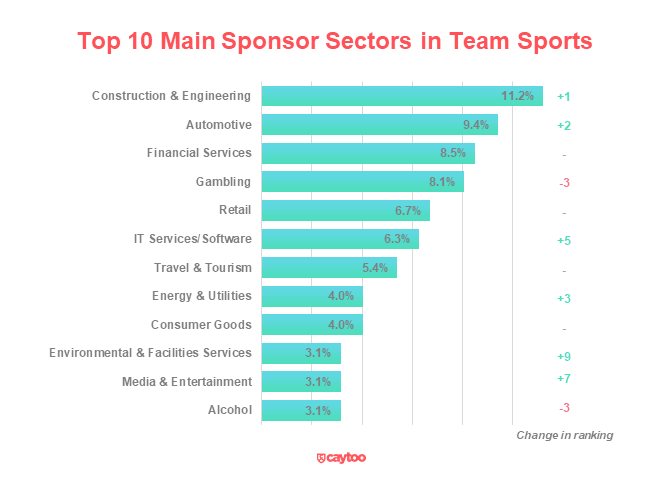

Our analysis of the leading 221 football, rugby and cricket teams now compared to two years ago has revealed that Construction & Engineering, Automotive and Financial Services have all overtaken Gambling as the most prevalent sponsorship sectors when it comes to a team’s main sponsor.

Gambling held top spot two years ago, accounting for 15.3% of all main sponsors, but this has nearly halved to 8.1%. This drop has been driven entirely by football where Gambling’s share has dropped by more than half from 32.7% to 15.2%.

Construction & Engineering firms now lead the way, accounting for 11.2% of teams’ main sponsors followed by Automotive (9.4%) and Financial Services (8.5%) firms.

Despite the drop, Gambling remains football teams’ most prevalent sponsor compared to Financial Services across rugby (union and league combined) and Automotive and Construction & Engineering, which jointly lead the way in cricket.

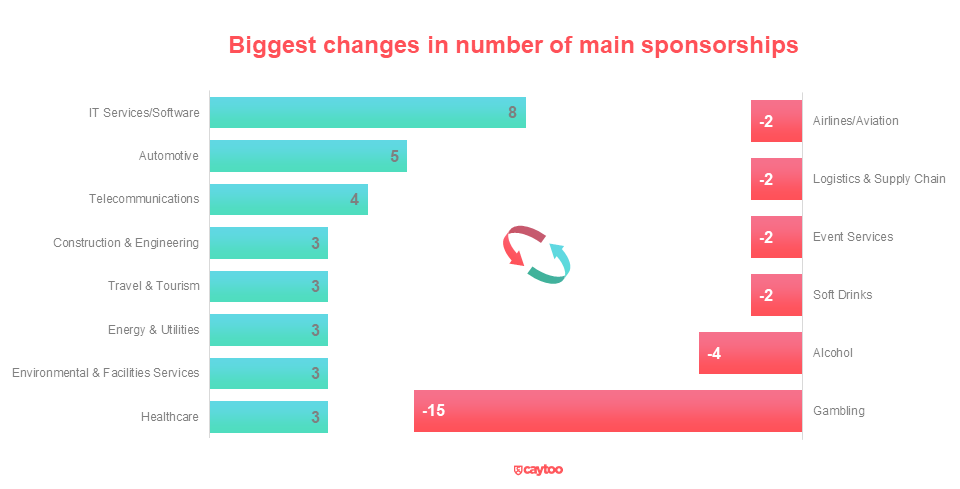

The demand to be more socially responsible has also resulted in Alcohol seeing the second biggest decline in prevalence behind Gambling, while Environmental Services and Healthcare are among those that have seen the biggest increases in prevalence.

A prime example of this change is Norwich City FC. At the beginning of our research the club signed a deal with Asian betting firm BK8 but by the time the research finished Norwich had terminated the deal due to public pressure over the sexualised nature of BK8’s marketing activity and replaced them with Norfolk-based Lotus Cars, who recently announced a £2.5 billion investment to move to producing only electric vehicles.

The shift to a digital world

The other major change in society reflected in the changing landscape of sponsorship is how the COVID-19 pandemic has accelerated the shift to a more digital world and the increasing dominance of companies operating in that space.

The IT Services/Software sector – which essentially help companies manage their IT and computer systems – has seen the biggest increase (+8) in the number of primary sponsorships, followed by the Automotive (+5, which has been driven by the online car retailers) and Telecoms (+4) sectors.

Interestingly, the increasing prevalence of IT Services/Software companies sponsoring sports has been almost entirely accounted for by women’s teams, which are responsible for six of the eight new sponsors. This makes the IT Services/Software the dominant sector among women’s teams, accounting for 18.4% of sponsors, and shows that female professional sport is seen as an increasingly important way for brands to gain exposure and recognition.

Overall, 24 sectors covered the 221 teams analysed, with the top five sectors accounting for 43.7% of sponsors and the top 10 accounting for 66.8%. Rugby is the most concentrated of the three sports around a few sectors; union’s three most prevalent sectors account for 45.7% of all sponsors, while in league its 45.4%. This compares to 36.0% in cricket and 34.7% in football.

These concentrations show the potential growth opportunity for rights holders and the sponsorship industry in general if they can start prospecting and looking to appeal to sectors and brands beyond the usual suspects.

By Alex Burmaster, head of research and analysis at ESA member caytoo

Visit the caytoo website to read the analysis in full – ESA members can email Alex to request free access to the report