• Gambling makes a “mini comeback”

• Financial Services and Alcohol see biggest decrease

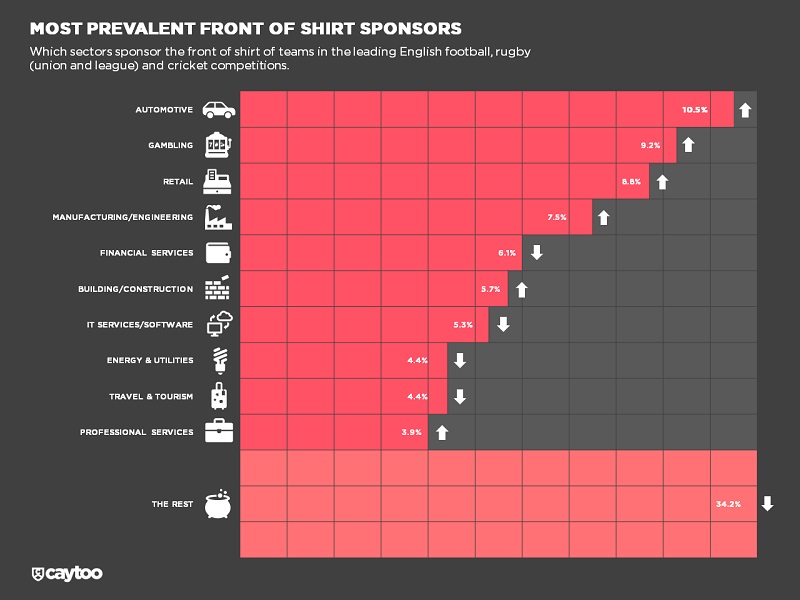

The Manufacturing/Engineering sector has seen the biggest increase in the number of front of shirt sponsorships across professional football, cricket and rugby teams in England.

The sector accounts for 7.5% of front of shirt (FoS) sponsors across 226 teams, up from 4.9% a year ago. It’s now the fourth most prevalent sponsor, overtaking Financial Services, IT Services/Software, Construction and Travel & Tourism, according to the latest annual study by sponsorship intelligence firm caytoo.

Retail (6.7% to 8.8%) is the next fastest-growing sector while Gambling has experienced a “mini comeback”, jumping back into second place (9.2%) as the joint third-fastest growing sector.

“It’s a notable return to favour for gambling after its share of sponsorships nearly halved from 2019 to 2021. However, this year, deals in rugby and cricket have resulted in a mini comeback which will surprise many as publicity on gambling sponsorship centres on football,” said Alex Burmaster, caytoo’s head of research and analysis.

“Indeed, reports say Premier League football clubs will vote on voluntarily banning betting firms from teams’ front of shirts. So the big questions are: will this happen and, if so, will other divisions or sports such as rugby and cricket follow suit?”

In contrast, Financial Services – last year’s second most dominant sector – has seen the biggest drop (down from 8.4% to 6.1%) and is now ranked fifth. The next biggest faller is Alcohol, down from 3.1% to 1.3% – just one quarter of the share it held three years ago.

Status by sport

Gambling remains football teams’ most prevalent sponsor (accounting for 15.4% of FoS sponsors) significantly ahead of Energy & Utilities (8.6%). Professional Services – whose share has almost quadrupled from 1% to 3.8% – is the fastest growing sector. In contrast, Construction has seen the biggest decrease – from a 9.5% share to 6.7%.

Automotive remains cricket teams’ most prevalent FoS sponsor and is also the fastest-grower; its share leapt from 13.1% to 17.7%, nearly double that of second-placed Travel & Tourism (9.7%). In contrast, Alcohol has seen the biggest decrease – its share tumbling two-thirds from 9.8% to 3.2%.

Across both rugby codes (union and league), Retail is the fastest-grower, jumping from 7.0% to a 13.3% share. Thus, it’s now the joint most prevalent sector along with Manufacturing/Engineering. In contrast, Financial Services – the most dominant sector across rugby last year – has seen the biggest decrease. Its share tumbling two-thirds from 15.8% to 5.0% and is now ranked joint sixth.

“The Covid pandemic meant digitally-led firms dominated last year’s fastest-growers but this year, with the exception of online car retail, has seen more traditional sectors leading the charge,” said Burmaster.

“It’s a reminder that chasing the next new thing isn’t always the best route when selling sponsorship. For instance, we frequently get requests to help find a fintech, crypto or online food delivery sponsor but we’re never asked to find a manufacturing or engineering one.”

-ENDS-